Market Commentary, July 30, 2020

Advance 2Q 2020 GDP Results - The Asterisk Next to Today’s Record

With the release of the advance 2Q 2020 GDP results, markets now have a more complete picture as to the full extent of the depth of economic upheaval resulting from the coronavirus and related shutdowns. The below is our attempt to contextualize the record-worthiness of the impact and offer another lens by which to consider the results.

Contextualizing Second-Quarter Results

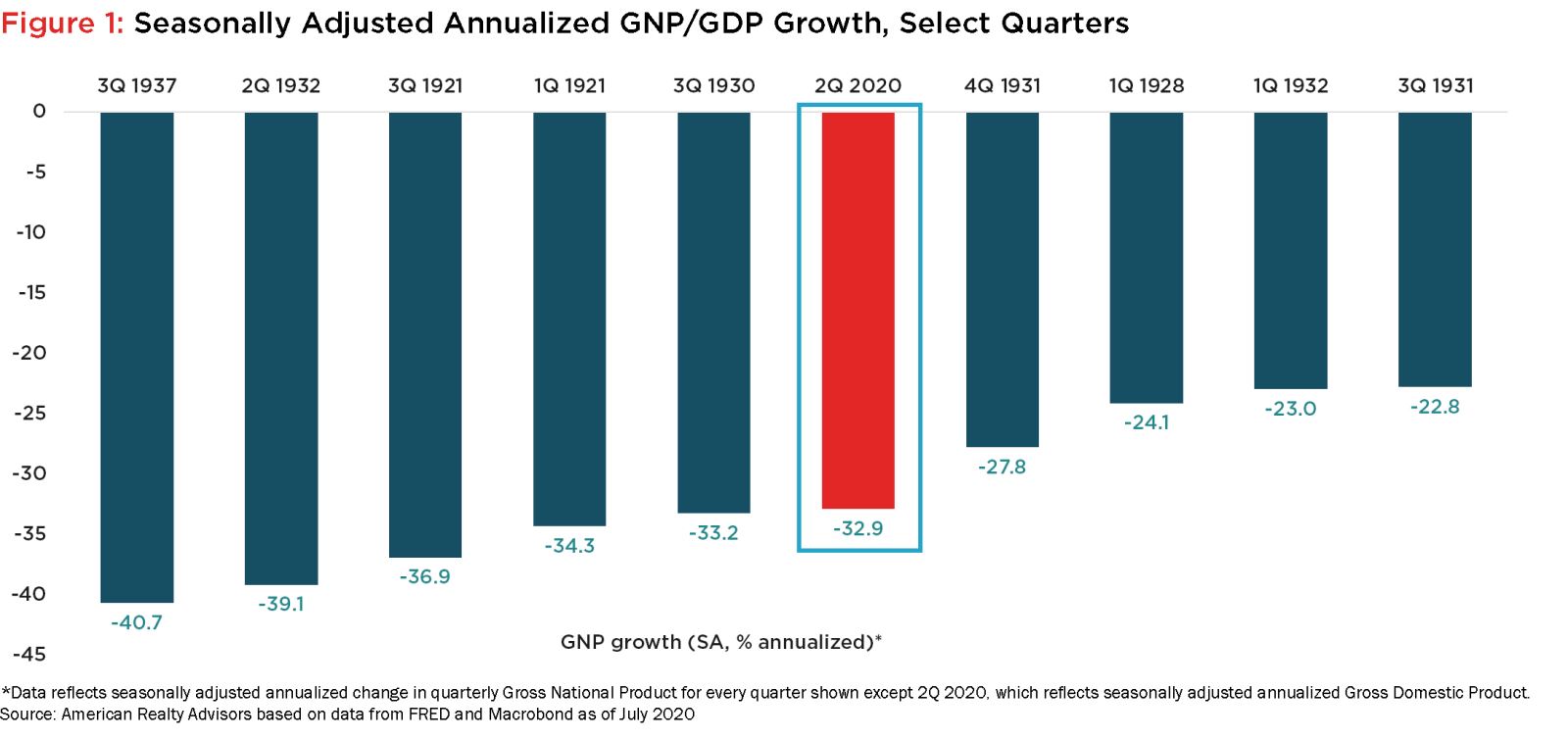

Advance estimates of second-quarter GDP reflect what many had already anticipated would be the worst of the economic hit. At a -32.9% seasonally adjusted annualized rate, the results have captured headlines as the worst quarterly period in U.S. history. While no doubt sobering, this designation is bit of a misnomer and has more to do with the historical limitations of official quarterly real GDP than it does actually being an unprecedented contraction.

Although not an exact methodological apples-to-apples comparison, leveraging the annualized seasonally adjusted rate of change in the Gross National Product (for which the Federal Reserve Bank of St. Louis has data stemming as far back as 1921), there have, in fact, been at least five quarters where the annualized contraction would have been more severe than our current results, had the methods of comparable tracking and reporting existed pre-1947 (Figure 1).

It is important to note here that these figures reflect how much GDP would contract if the quarterly rate of change were sustained for a full year – that is, if the contraction experienced in the second quarter were to continue over the next three quarters. Yet as many acknowledge, the worst of the economic impact occurred in April, when wide swaths of the American population were in various stages of quarantines and shelter-in-place mandates, and that May and June by comparison reflected positive momentum. This suggests that viewing the coronavirus impact solely through the lens of annualized figures may be a bit misleading, as it is unlikely the next three quarters will mimic the last to the same degree.

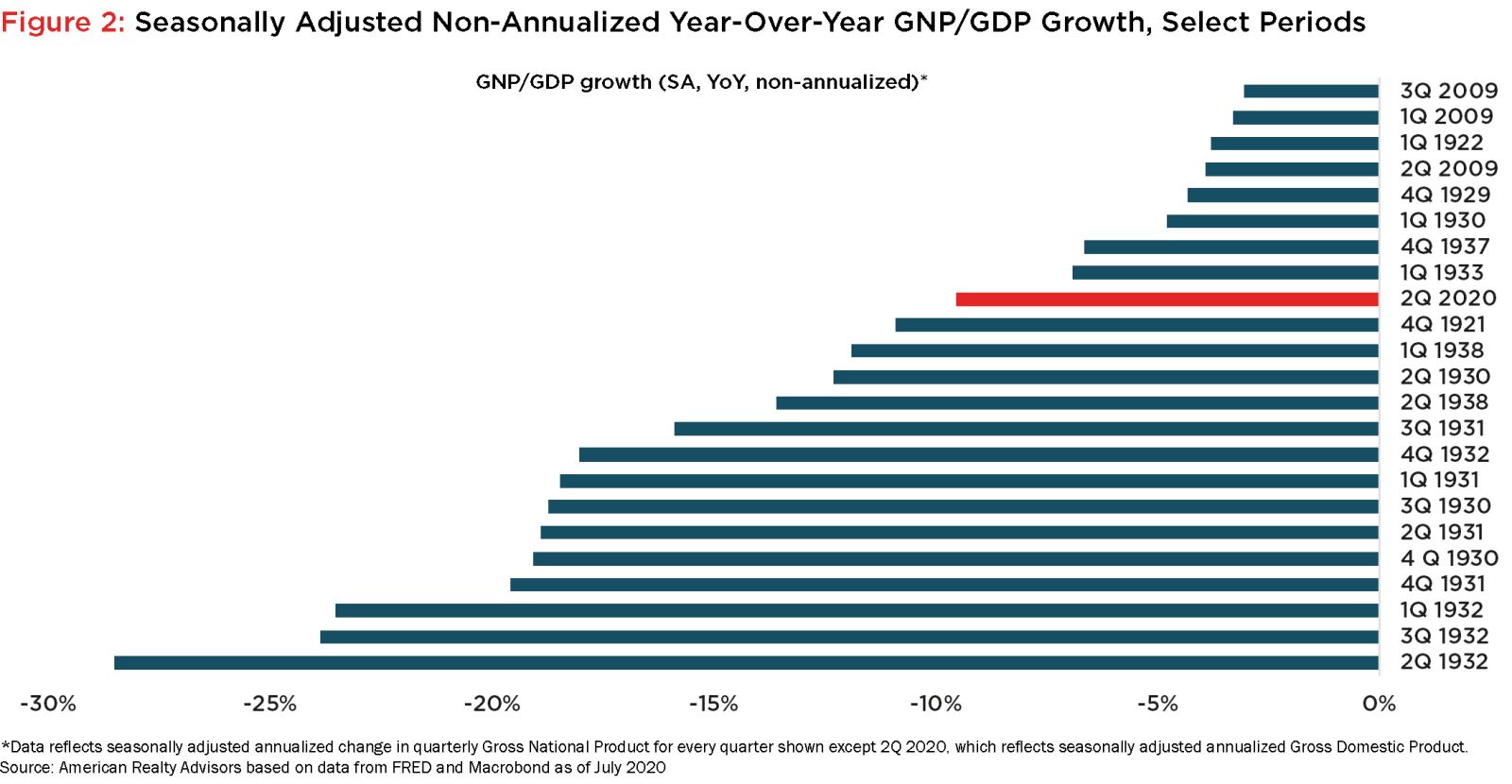

Were we to just look at GDP results in the second quarter relative to the same period one year prior (on a non-annualized basis), we would see that the contraction totaled nearer to 9.5% (Figure 2); against a similar historical backdrop (again, using our GNP series as proxy), there were at least fourteen occurrences whereby the year-over-year contraction recorded was significantly worse (Figure 2).

Conclusion

We are by no means claiming that the impacts felt in the second quarter were nothing short of debilitating – even on a non-annualized basis, the latest contraction was still 3x worse than any quarter’s year-over-year decline during the Global Financial Crisis. And while the pace of improvement in the latter half of May and June was encouraging, the resurgence of coronavirus cases in many U.S. cities portends a slowdown in the pace of reopening and rehiring. We believe the third quarter will look much improved by comparison; yet with momentum abating, we anticipate the U.S. is in for a slower recovery marked by starts and stops dictated by the trajectory of the virus.