Real estate has long served as a cornerstone of institutional investment portfolios, offering income, inflation protection, and a structural diversification from the classic stock-bond starting point. As portfolios have evolved, so too have the ways in which investors can access real estate, with both public and private having a role to play. This primer examines both ways to access real estate on their own terms, before comparing the two across key dimensions that we believe matter more to long-term investors.

Public Real Estate: Overview, Benefits, and Drawbacks

Real estate investment trusts, more commonly known as REITs, are publicly traded companies that own, operate, or finance income-producing real estate across the various property sectors. They trade on major exchanges similar to traditional stocks, providing investors with real estate exposure that can be traded and rebalanced daily. While this liquidity is often a key reason for its inclusion in portfolios, it often leads to wider swings in valuations that may not always reflect real estate fundamentals on the ground. Understanding the benefits and drawbacks is important when considering adding this allocation.

Benefits of Public Real Estate:

- Liquidity: REITs can be liquidated quickly at the prevalent daily stock price, providing a backstop for near-term liquidity events and allowing for dynamic rebalancing.

- Transparency: Public REITs file regularly with the SEC, providing standardized financial reporting, governance disclosures, and audited financial statements that are available to the public. This can simplify due diligence relative to private vehicles.

- Income distribution: The mandatory distribution (by law, REITs must distribute at least 90% of taxable income to shareholders) supports ongoing income returns, relevant for institutions with ongoing capital needs.

Drawbacks of Public Real Estate:

- Higher volatility: Because REITs trade continuously in public markets, they can be prone to larger swings related to equity risk sentiment irrespective of current supply-demand fundamentals.

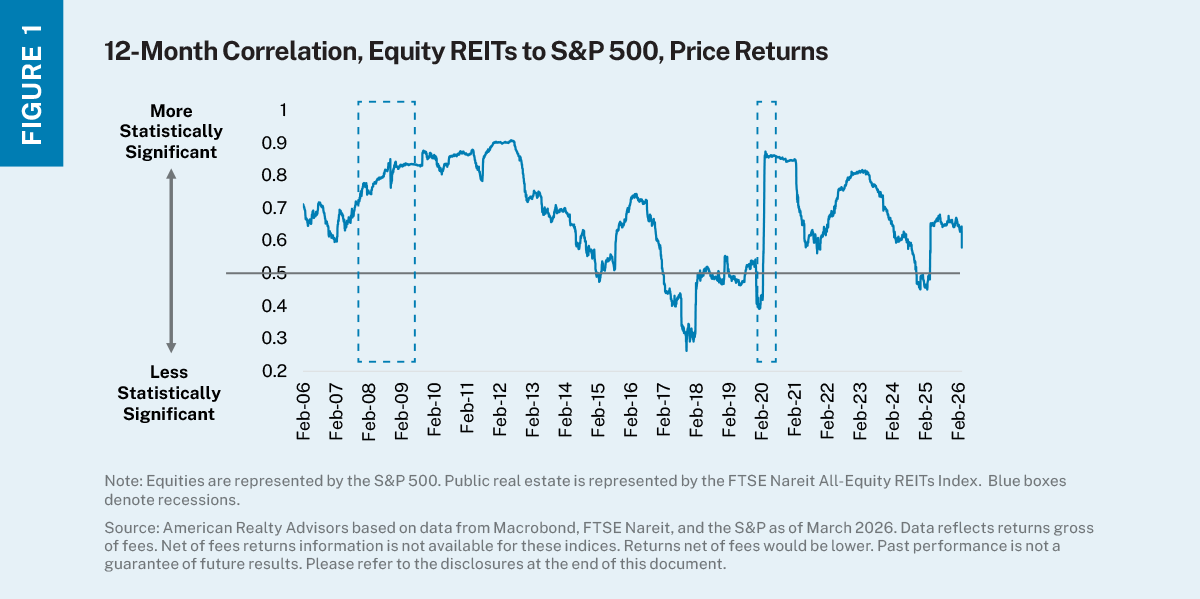

- Equity market correlation: Over the short term, REITs behave more similarly to the broader stock market than the real estate itself, which can lessen diversification benefits. During periods of market stress, REIT correlations to the S&P 500 have historically spiked, reducing diversification benefits precisely when they are needed most (see Figure 1).

- Limited customization: REIT investors have little influence over the REIT strategy. There is no mechanism to tilt towards specific markets, lease structures, or business plans without stock-by-stock active management, which can introduce its own complexities.

Private Real Estate: Overview, Benefits, and Drawbacks

Investing in private real estate for institutional investors often comes in the form of investments in commingled funds. Private real estate managers form funds that aggregate capital from numerous investors with the intention of directly owning and managing properties. Returns are derived from rental income, lease escalations, and asset appreciation, rather than from daily market pricing. For many, this is considered the “pure play” real estate approach that most closely emulates true property exposure.

Benefits of Private Real Estate:

- Variety and customization: Funds can span strategies, from income-oriented, lower-risk, open-end core to closed-end value-add or opportunistic vehicles that have finite terms and take on higher risk with the goal of achieving higher returns. Some investors may also opt to create separately managed accounts (SMAs) with managers, which allows the investor greater influence over strategy – targeting specific property types, geographies, and risk profiles.

- Lower volatility and correlation: Because private real estate is valued using appraisal-based methodologies – income capitalization and comparable transaction analysis – it typically exhibits lower measured volatility and reduced correlation to public equities.

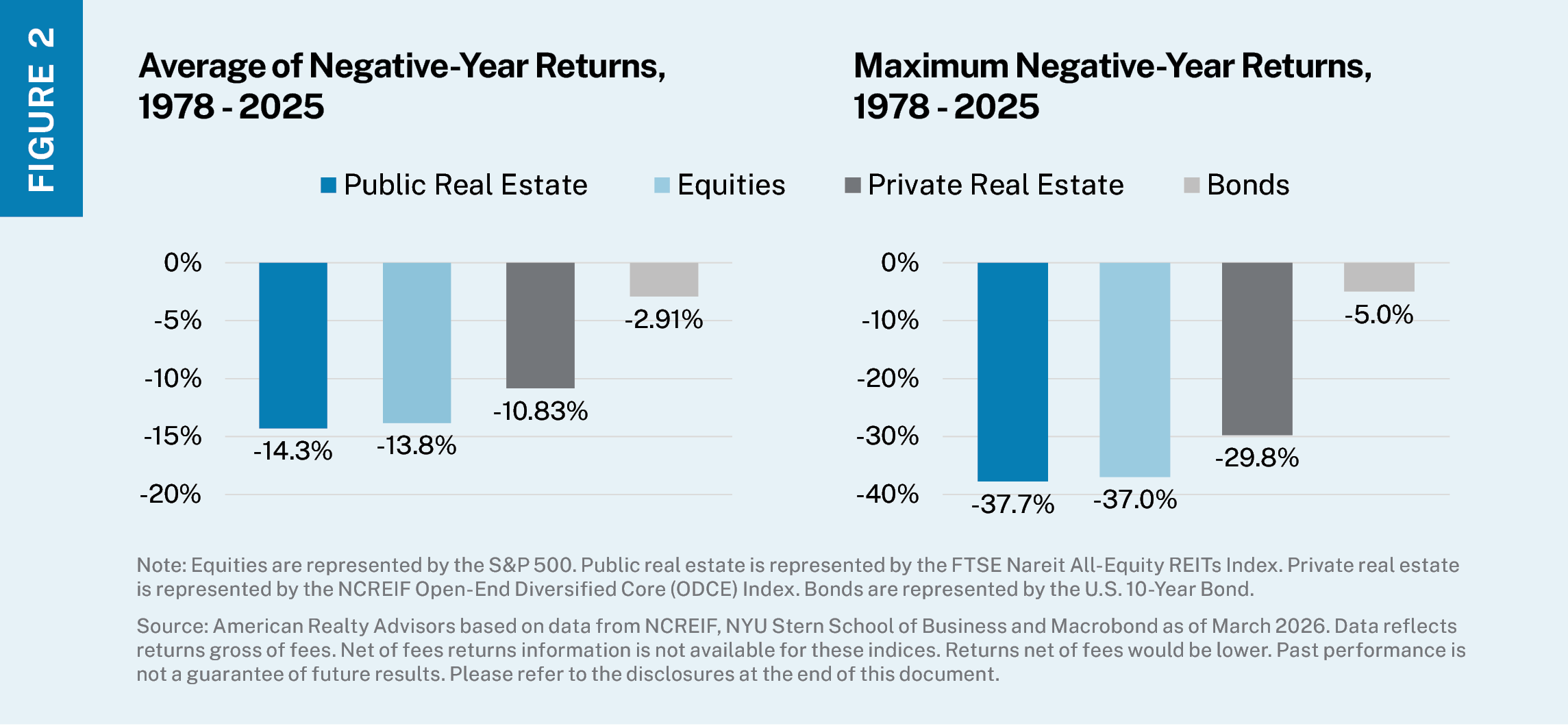

- Lesser downside: Compared to public REITs, private real estate’s average and maximum negative-year returns going all the way back to 1978 show private real estate offers compelling relative downside protection (see Figure 2).

Drawbacks of Private Real Estate:

- Illiquidity: Capital committed to private real estate is usually locked up for a number of years. Distributions depend on asset performance and manager discretion, and while some vehicles offer liquidity intervals, market conditions may create scenarios whereby redemptions are not satisfied immediately.

- Valuation lag: Appraisal-based valuations, while smoothing reported volatility, can also take time to catch up in periods of rapidly shifting market conditions.

- Manager risk and due diligence burden: Unlike public REITs with uniform disclosures, private vehicles can vary significantly in reporting quality, governance, and fee structures. Manager selection is consequential – return dispersion between top- and bottom-quartile managers is substantially wider than the dispersion in public markets. As such, operational due diligence demands on pension plans and their consultants tend to be correspondingly higher.

Comparing Public and Private Real Estate

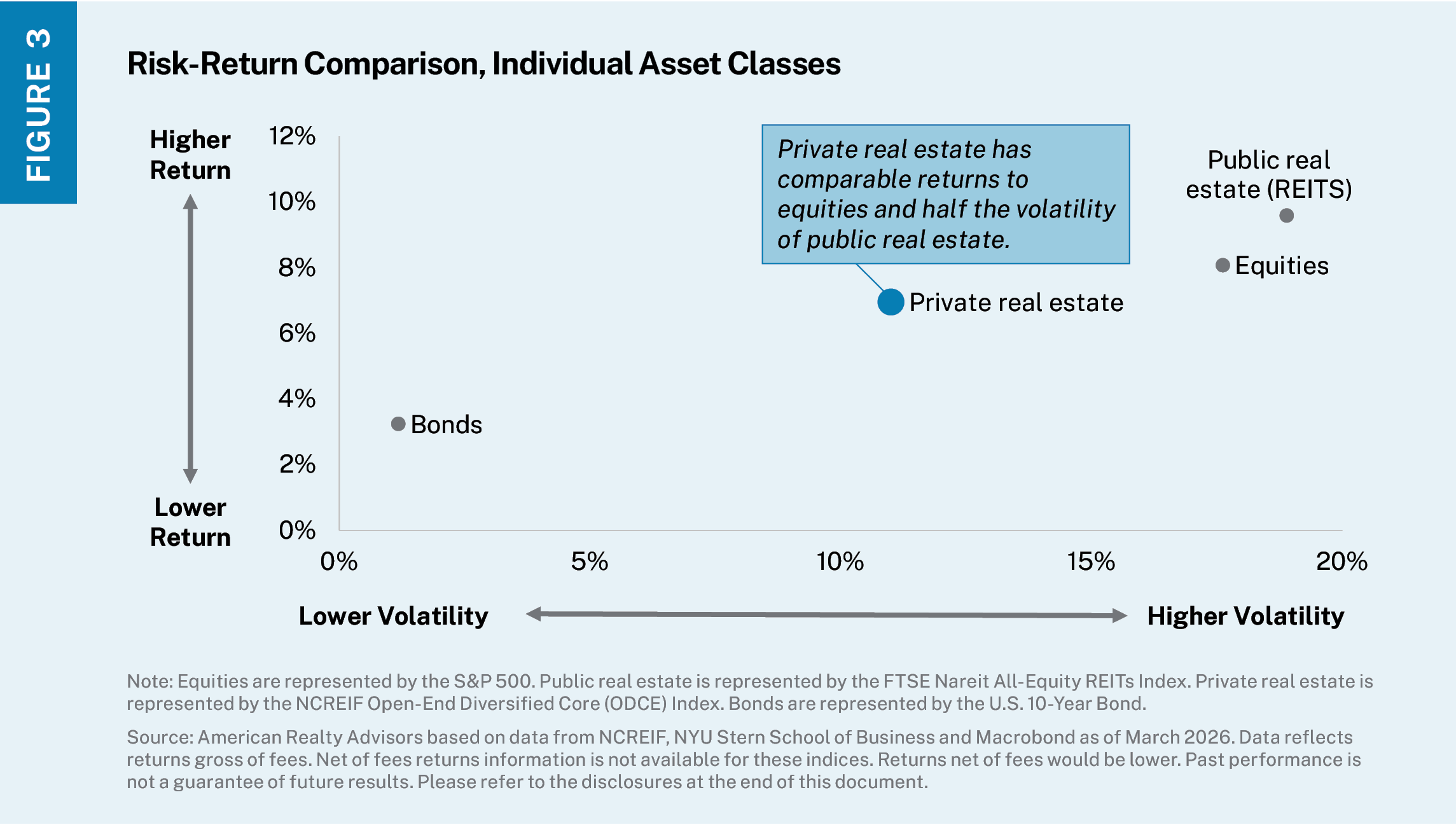

Over long time horizons, private real estate has generally outperformed public REITs on a total return basis, with lower measured volatility – producing a meaningfully better Sharpe ratio (a measure of how much additional return an investor receives per increased risk). NCREIF data for core private real estate funds and FTSE Nareit data for equity REITs both reflect this pattern across multiple decades, though relative performance can vary by time period, cycle, and property sector (see Figure 3).

It bears noting that private real estate’s volatility benefits from appraisal smoothing, which can understate true volatility. Unsmoothed private real estate returns often show higher volatility than headline figures suggest, though even so, may still be materially lower than REITs in most periods.

To truly compare these two sides of the real estate coin, we offer three considerations for investors:

- Correlation and Diversification

This is arguably where the structural distinction between the two vehicles is most consequential for portfolio construction. REITs, as publicly traded equities, show higher rolling correlations to the S&P 500 than private real estate, a correlation that rises in down markets. Private real estate, by contrast, has exhibited low and relatively stable correlation to both equities and bonds, contributing genuine portfolio diversification benefits rather than equity-like exposure with a real estate label. - Liquidity vs. Returns

The liquidity spectrum between REITs and private real estate is wide and largely binary. REITs offer intraday liquidity at whatever the market-clearing price is; private funds can address redemptions generally at their discretion. At the soonest, redemption requests may be satisfied the next quarter, though the most recent period has demonstrated that some funds will elect to put up exit queues and pay a portion of distribution requests over years to avoid “fire selling” fundamentally good assets to satisfy liquidity.

For institutions with longer-term investment horizons, such as pension plans and endowments, accepting this illiquidity in exchange for the associated premium and diversification benefits is often an acceptable tradeoff. - Portfolio Construction Implications

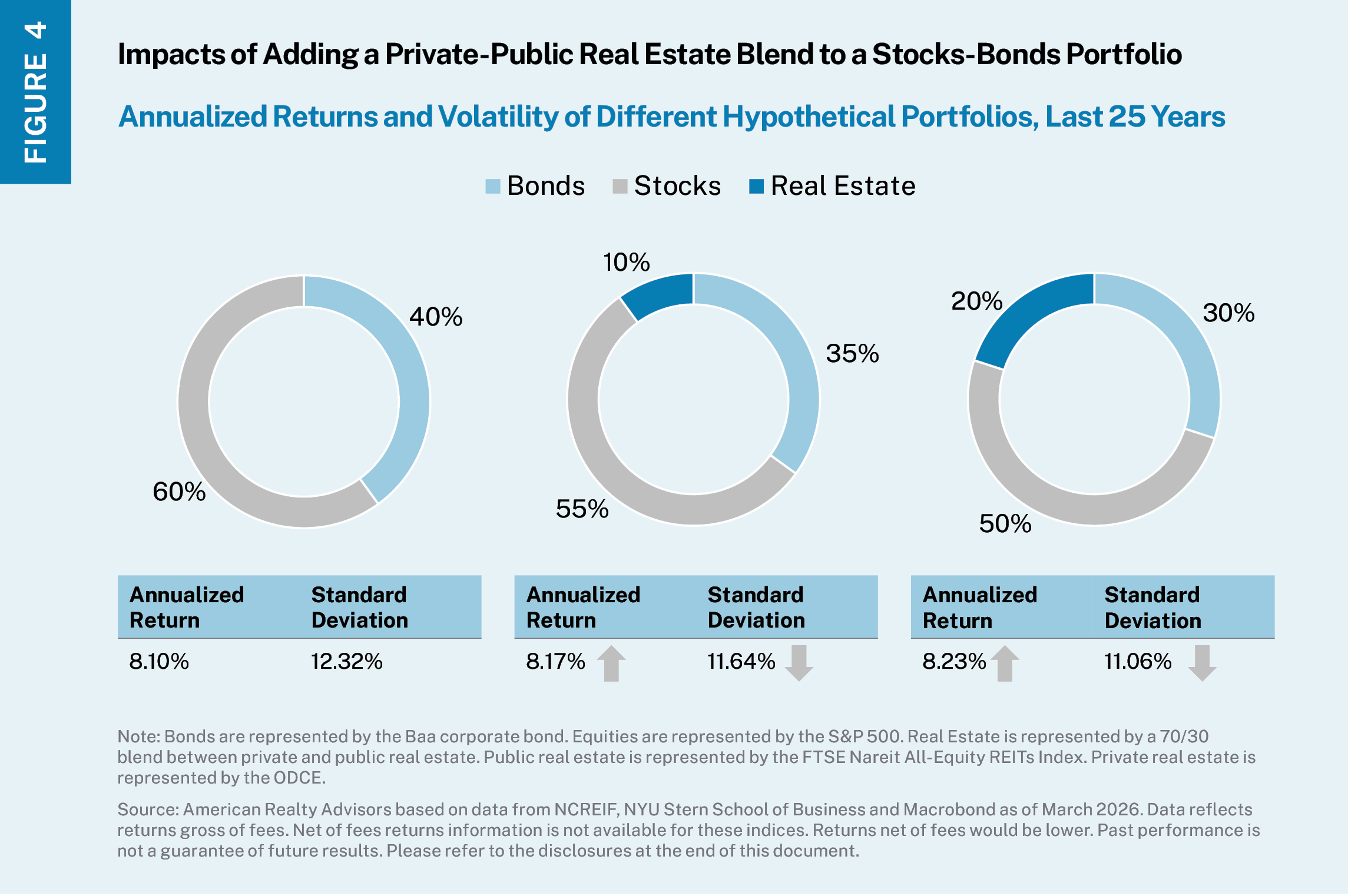

For most institutional allocators, the question is generally not private real estate or REITs, but rather how to size the two within a broader portfolio context. We believe a reasonable framework is to use private real estate as the anchor, adding the “truest” real estate exposure and gaining the income, diversification, inflation protection and downside mitigant, and then leveraging REITs as the liquid sleeve of the broader real estate allocation. The data suggests adding 10 to 20% real estate to a stocks-bonds portfolio enhances returns and lowers volatility, with the real estate being a 70/30 blend of private and public (see Figure 4).

Private real estate offers the exposure to fundamental return drivers, genuine diversification, and lesser volatility that public markets, by their nature, dilute. For institutional investors with the horizon and structure to access both, an intentional combination is likely the best example of what real estate can contribute to a portfolio.

House View H2 2026