Halfway through the second quarter, the U.S. economy continues to resist easy characterization. Ask 10 economists how things are going, and you will likely get 10 different answers, not because they are looking at different data, but because the data itself is pulling in 10 different directions.

Start with some of the headline numbers, and the picture looks encouraging. The economy grew at a healthy 2 percent clip last quarter; dig a little deeper, though, and you’ll find that roughly half of that growth came from a surge in business investment in AI, a powerful but narrow engine that isn’t likely to carry the same weight going forward. That means the economy will need to lean on its primary engine, consumer spending. The problem is that consumer spending has begun to slow, as rising prices are taking a bigger bite out of household budgets. The government’s latest measure of consumer prices jumped to 3.8 percent in April, a move that doesn’t go unnoticed at the grocery store. Compounding this pressure is the situation with oil. The Iran conflict has sent gas prices soaring, with Americans spending $125 million more at the pump in a single day compared to just a week prior.1 Even in the most optimistic scenario, analysts expect oil prices to remain elevated for the remainder of the year. For consumers already feeling the pinch of rising prices, more money spent at the pump means less available for everything else, from groceries to rent to the discretionary spending that keeps the broader economy moving.

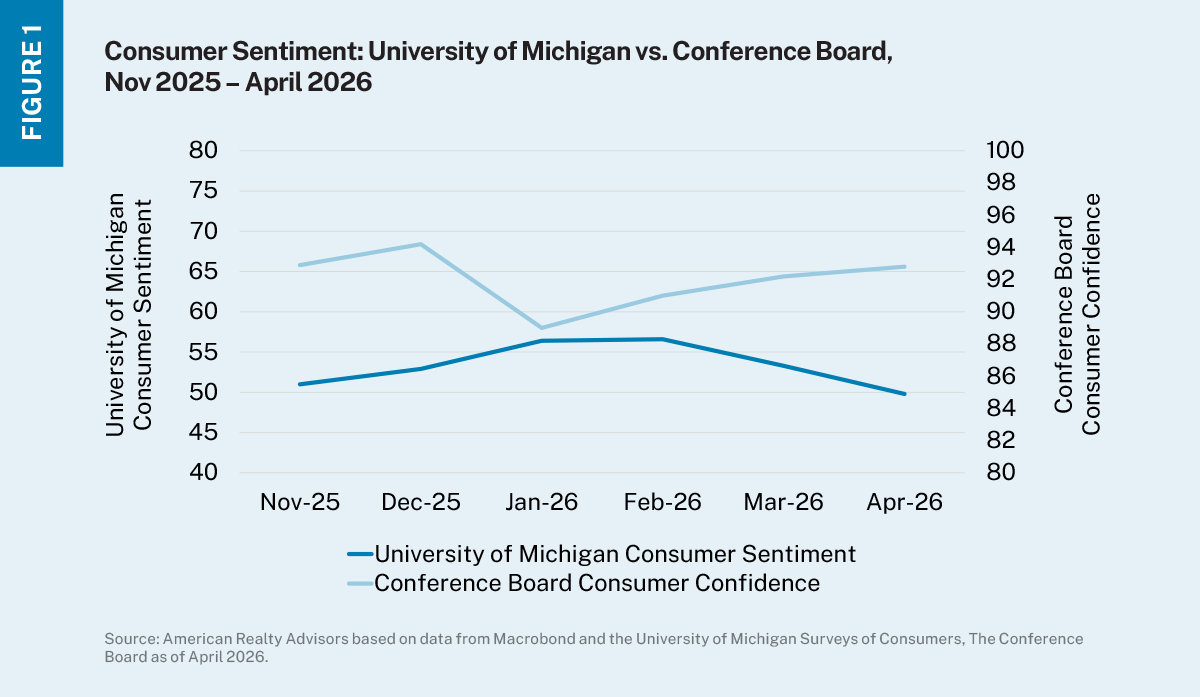

And ultimately the labor market simply doesn’t have the capacity to offer any meaningful relief at the moment. While two consecutive months of better-than-expected job gains is an encouraging sign, the bulk of those gains continue to come from a concentrated set of industries, and underemployment is actually rising (that is, more Americans taking part-time work because they simply can’t find full-time positions). We are stuck in what economists have been calling a ‘low-hire, low-fire’ environment, where people aren’t losing their jobs (a net positive), but they are not easily finding new or better-paying ones either (net neutral). All of this is showing up in how people feel about the economy, though even that is hard to pin down. Two of the most widely cited consumer sentiment surveys were released the same week and told seemingly different stories. The University of Michigan’s reading hit an all-time low, while the Conference Board’s came in above expectations (Figure 1). Same week, same economy, yet two completely different reads depending on where you are looking.

A Deeper Look into the Fed

Perhaps the most telling sign of just how complicated this picture has become is that even the Federal Reserve, the institution specifically charged with making sense of it all, appears to be struggling to reach consensus. At their latest meeting, the Fed voted to hold interest rates steady for the third consecutive time. But what made this meeting notable was not the decision itself; it was the level of disagreement behind it. The vote came in at 8-4, the highest level of dissent among Fed governors since 1992. The split was not simply about timing, it was about direction, with some governors wanting to cut rates (to help support the consumer and stimulate the jobs economy) while others did not even want to leave the door open to that possibility.

The Fed finds itself in an uncomfortable position where every available option carries a meaningful cost. Cut rates and you risk stoking the flames of inflation that is already running well above target. Hold, as they chose to do, and the economy remains stuck in the kind of stagnation that has defined the moment. And raising rates, while not off the table entirely, risks breaking something in an economy that doesn’t appear strong enough to absorb that kind of pressure right now.

CRE Implications

Put all of that together and what comes out on the commercial real estate side is a market that keeps stopping and starting. Not because the fundamentals are broken, nor because the capital is not there, but because investors cannot seem to get a clear enough read on what is coming next to transact with confidence.

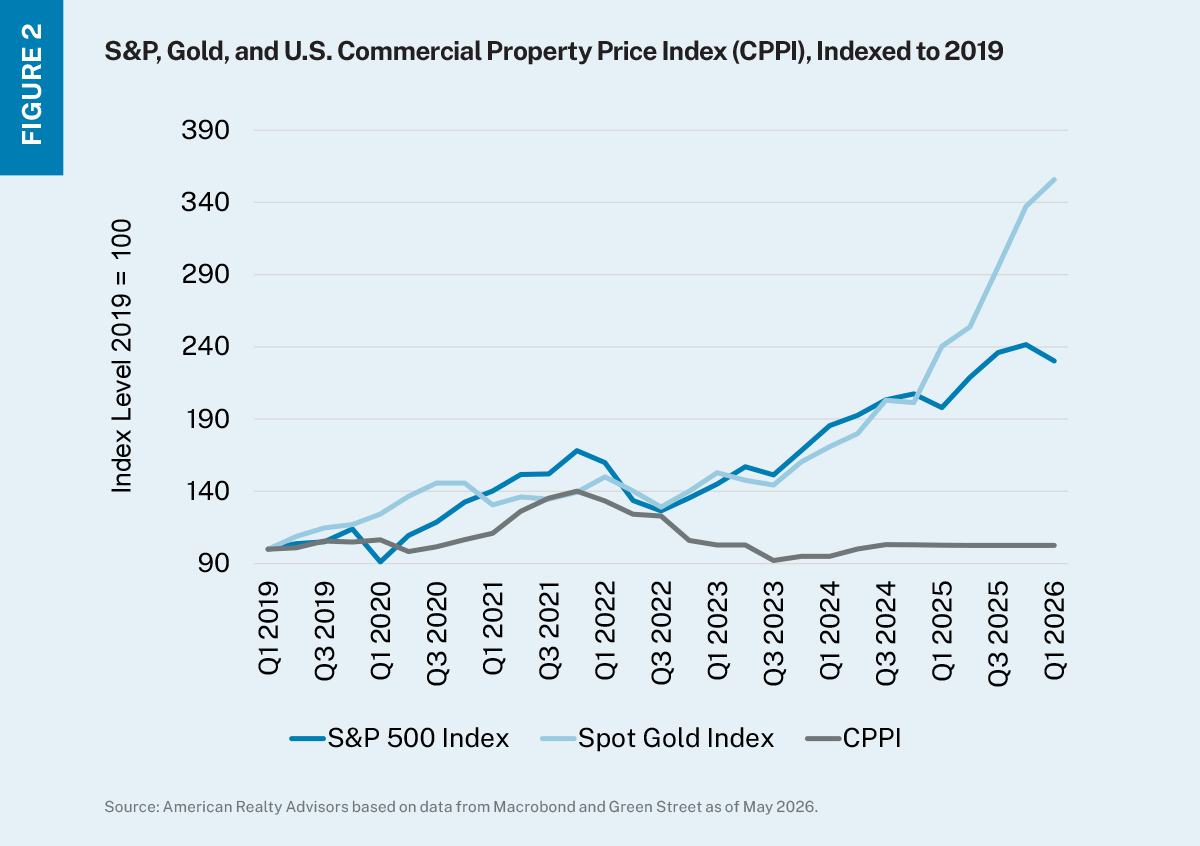

Commercial real estate entered the second quarter of the year with real momentum – transaction volume is up 23% year-over-year, debt markets are healthy, and if anything, lenders have more appetite for deals than the market is currently giving them.2 But that momentum keeps getting interrupted every time the macro picture shifts. The irony in all of this is that the opportunity sitting underneath all of this noise hasn’t shifted. Values have repriced 20-25% from their 2022 peak, and while it is true that the recovery off that bottom has begun, the asset class is still trading at a meaningful discount relative to other asset classes (Figure 2). The only thing standing between this recovery and a faster pace is certainty, and that’s the one thing the current environment is not yet offering.

While the macro picture might not clear up on anyone’s preferred timeline, opportunity in commercial real estate doesn’t require a perfect backdrop. What is required is the discipline to recognize that the asset class has already absorbed its reset, the capital is staged and ready, and the investors who are willing to underwrite to today’s reality rather than wait for yesterday’s certainty are likely to be the ones who look back on this moment as the right time to have moved.

House View H2 2026