Just a month into the first quarter, the economic picture has become more complex. Fourth-quarter GDP growth slowed to an annualized 1.4% in Q41 amid the late-year shutdown, while January employment surprised to the upside, even as revisions tempered prior years’ gains. Still, consumer confidence has fallen to a 12-year low,2 reflecting persistent unease about the jobs market and income prospects, despite pockets of resilience in the data.

This disconnect – between the “market” and peoples’ realities – is a challenge for policymakers. In the January 28th meeting, Fed governors voted to hold short-term interest rates steady, quoting stabilizing unemployment and healthy consumer spending as rationale for maintaining a neutral policy stance.

The throughline over much of the last 18 months has been this idea of a two-speed, or “K-shaped” economy, and that remains in play at the start of 2026. A narrower set of industries and households appear to be doing well, while others struggle to regain momentum, creating what we believe to be asymmetric risk and opportunities when it comes to the investment landscape.

Implications for Real Estate

A widening gap in where growth originates from complicates the macro backdrop in a way that we believe matters for rates and asset pricing. Labor market slack has risen at the margins, and real income growth has slowed, and yet demand remains firm enough to keep inflation from falling more decidedly back to target. We believe this tension helps explain why policy has not been eased further (yet) even as parts of the economy are showing signs of fatigue.

That backdrop has important implications for capital markets and real estate returns. When demand holds up despite slower income growth, markets tend to price a longer period of policy rate stability rather than a rapid easing cycle – in short, less reason to believe in a quick return to cap rate compression as a major return driver. The positive to this for investors is that there should be less dramatic moves in benchmark rates, allowing for the ongoing stabilization in real estate capital markets to continue. It also means that returns may become more dependent on capital structure, lease duration, and cash flow resilience rather than cyclical acceleration, which should favor groups that are cycle tested and focused

on operations.

More broadly, a consumption-led expansion supported by balance sheets rather than income tends to favor selectivity over beta. This suggests a greater need to position assets to best capture demand from the narrower set of households and industries that are expanding, be that for residential rental product or commercial office or industrial space. For real estate investors, this environment is likely to reward assets aligned with income-resilient tenants and markets with durable and expanding employment bases (think: education, health services, tech).

Growing Consumer Divide

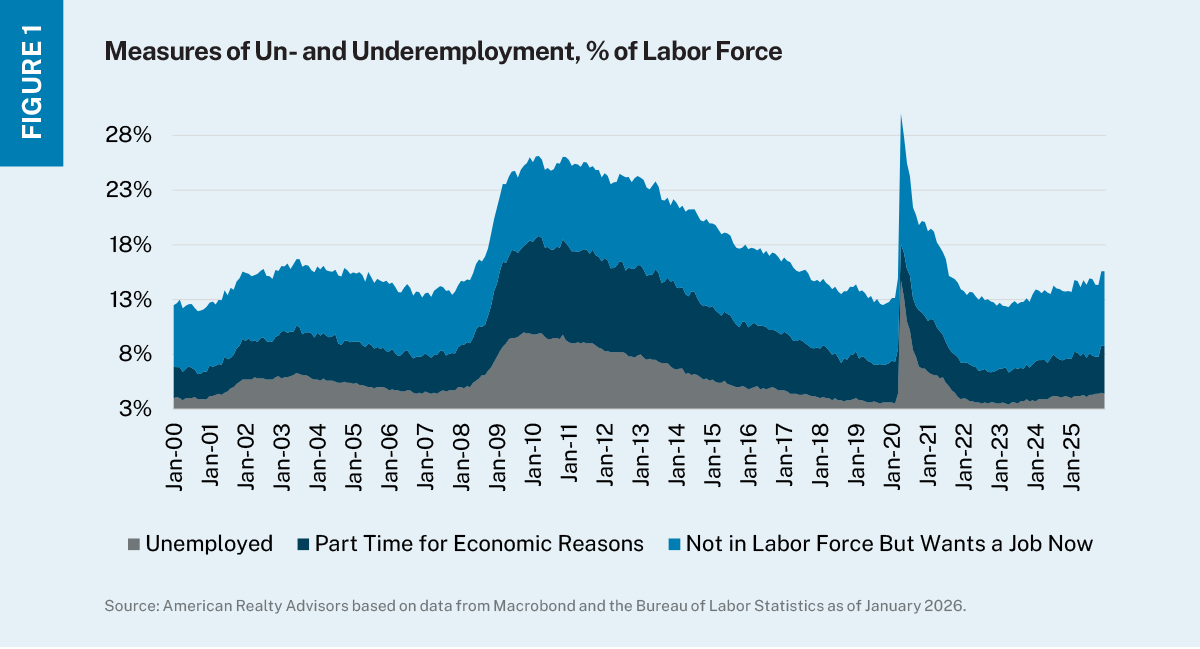

Unemployment is one of the primary things considered by Fed policymakers when it comes to determining which direction to go with interest rates – too high, they will be prompted to cut to reinvigorate the economy and spur hiring; too low, wages and prices may start to overheat. Overall unemployment as of December stood at a relatively low 4.4%, a 0.1% improvement from December and on par with September and October.3 So why then are so many consumers deeply unhappy?

The answer may lie beneath the surface. Though overall unemployment remains low by historic standards, there are 7.5 million people unemployed and an additional 10.2 million people who are either under-employed or have left the job market entirely even though they want to work (Figure 1).3 Combined, these categories equate to 19.5% of the total domestic labor force, a not-insignificant factor when we think about consumers’ collective ability to continue to support the economy.

On the surface, spending still looks resilient. Households are buying and spending in ways that do not resemble a traditional slowdown. But underneath the headline strength is a consumer base increasingly being split into two groups. On one hand, there are the households struggling to find work or stuck in jobs that don’t fully cover their costs, while another cohort – higher-income, asset-owning households – continues to spend comfortably. This widening gap is increasingly visible and is one of the key areas we are focused on for 2026.4

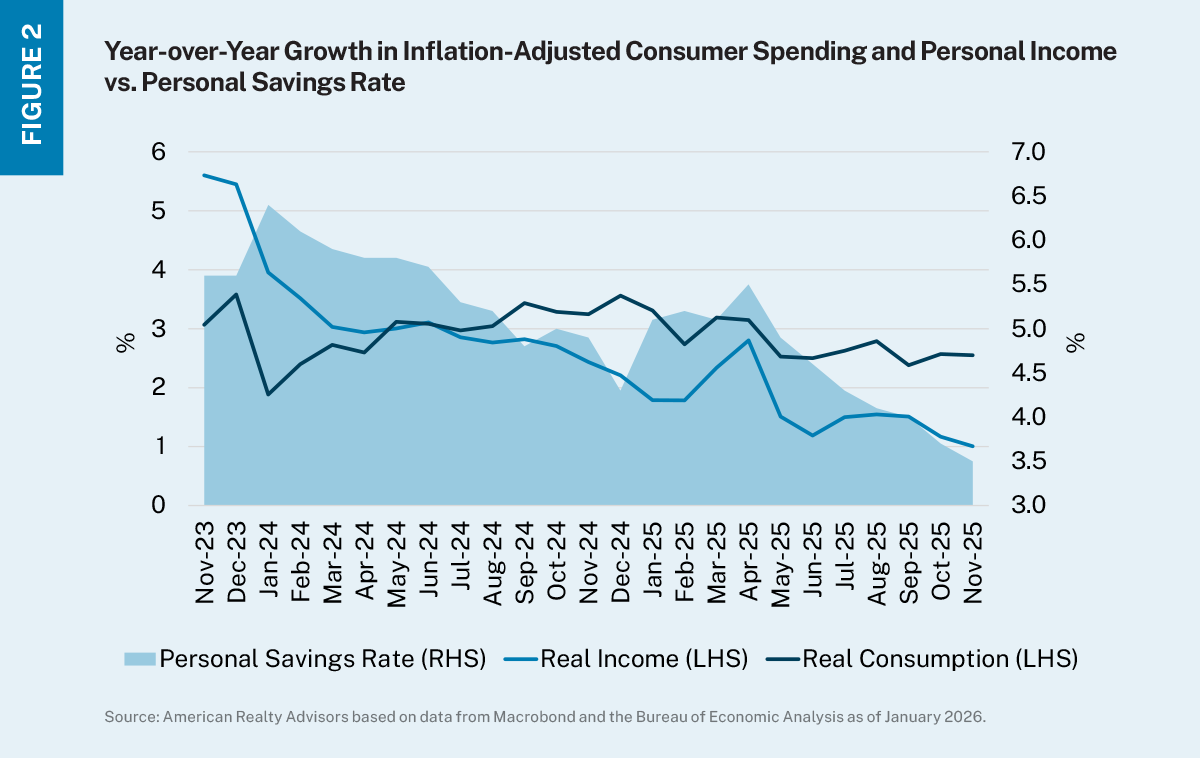

This appears to be materializing in the gap between consumer spending growth and income growth. Year-over-year real consumer spending growth has outpaced disposable income growth for 17 consecutive months, while at the same time, personal savings has fallen to its lowest level since October 2022 (Figure 2). While using savings isn’t necessarily a negative (savings are meant to be used at some point), the timing matters. Households are drawing down buffers not after a shock (like what we saw after the pandemic), but to offset persistent cost pressures and uneven income growth. If savings are depleted, households may have no choice but to cut back, which would be negative for the economy.

Taken together, these trends point to a consumer that is increasingly bifurcated. Aggregate spending can and has remained strong even as a growing segment of households becomes more vulnerable. That dynamic helps explain why the economic story feels contradictory – resilient at the top, strained underneath – and why there remains a lingering caution even as GDP growth looks robust.

In environments with two different paths, capital needs to become more selective. Assets with durable income and defensible demand drivers are likely to be more attractive than those whose business plans and underwriting are reliant on riding a recovery wave. We believe the current real estate cycle will be defined less by the parts of returns that come from the market moving up or down as a whole, and more by differentiation.

Mid-Quarter Economic Pulse: Q2 2026