Population trends tend to shift slowly, but recent growth patterns will require increased focus on market and asset selection for multifamily investors. Long-term strategy should factor in emerging shifts in the U.S. population, as well as what is driving them.

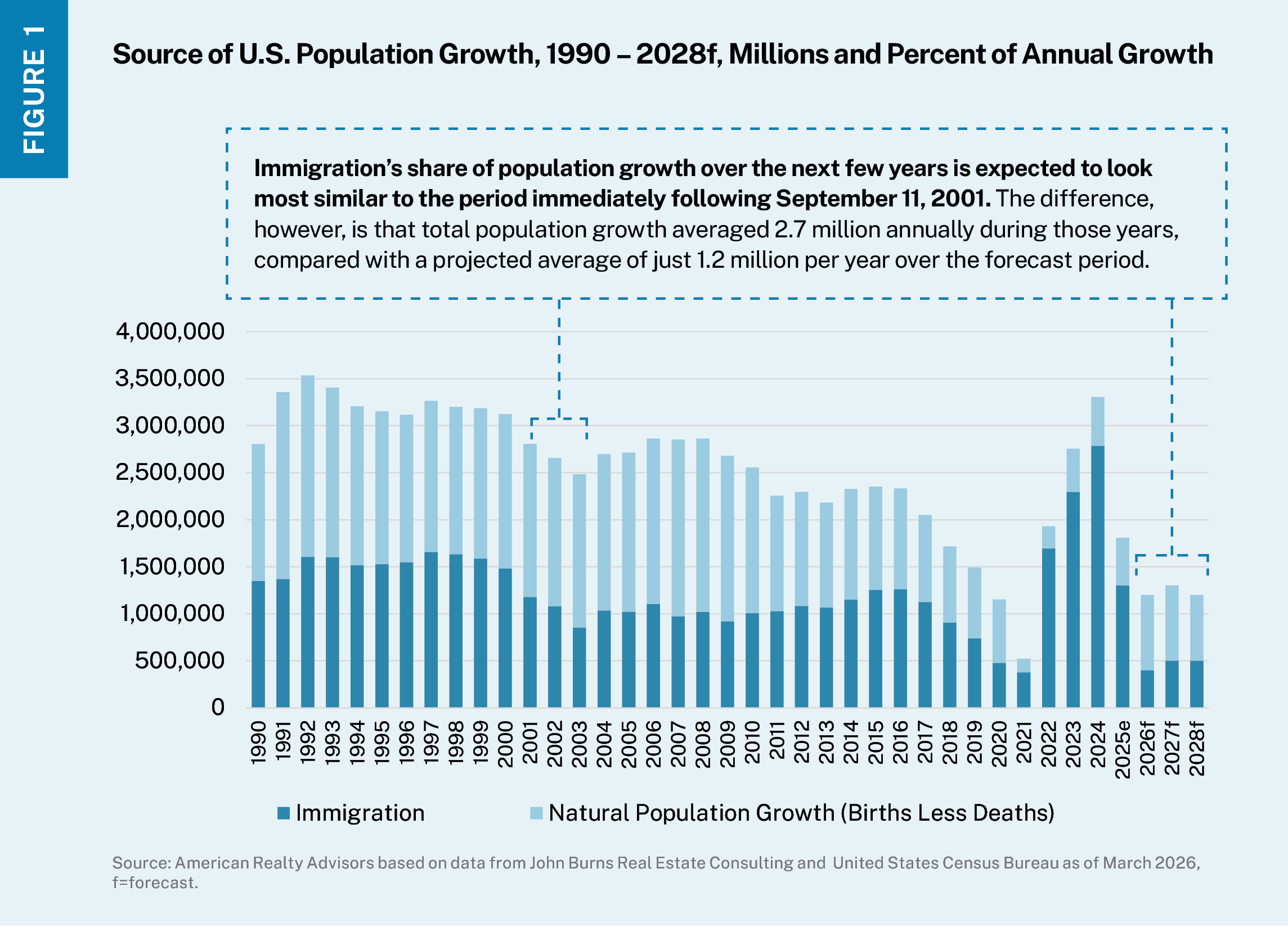

Natural population growth has slowed materially over the past decade as Americans are having fewer children and the Baby Boomer generation ages. In turn, immigration has increasingly accounted for more of overall population growth. Between 2010 and 2020, immigration represented just under half (45%) of overall population change in the U.S., increasing even more dramatically during the years following the pandemic. Between 2022 and 2024, immigration accounted for more than 80% of net population growth (Figure 1). Without immigration in that period, overall population growth would have been minimal.

Prior to recent changes in policy, immigration was expected to drive roughly two-thirds of annual population growth over the next five years. However, the latest projections suggest those inflows may be closer to half of earlier estimates. Combined with already low growth expectations, we are seeing a shift that has direct implications for the economy overall and for real estate markets.

For multifamily housing, that effect is straightforward. Slower net population growth tends to translate into fewer new households, which is the foundation of apartment demand. In recent years, elevated immigration added renters beyond what natural population growth alone would have produced. That extra demand helped many markets absorb new supply, particularly in gateway markets such as New York, Los Angeles, and Miami that are prime destinations for new entrants into the country. This migration impacts the “non-institutional” apartment space first, as a decent share of immigrants tend to live with family or in smaller, less-costly buildings upon arrival versus renting Class A apartments with stricter approval qualifications. However, the impacts make their way to institutional properties eventually, as fewer new entrants into the country means fewer go on to move up the rental curve and eventually become Class A renters.

While the pace of household formation is likely to slow alongside moderating net population growth, that does not imply an immediate reversal in renter demand. It does suggest, however, that capturing demand will depend less on broad migration tailwinds and more on asset selection, location quality, and competitive positioning. In markets with sizable development pipelines, even a modest slowdown in household formation can stretch lease-ups, increase concessions, and weigh on effective rents. In markets where supply is more contained, the adjustment may be less pronounced, though rent growth is still likely to settle closer to long-term norms rather than prior-cycle highs.

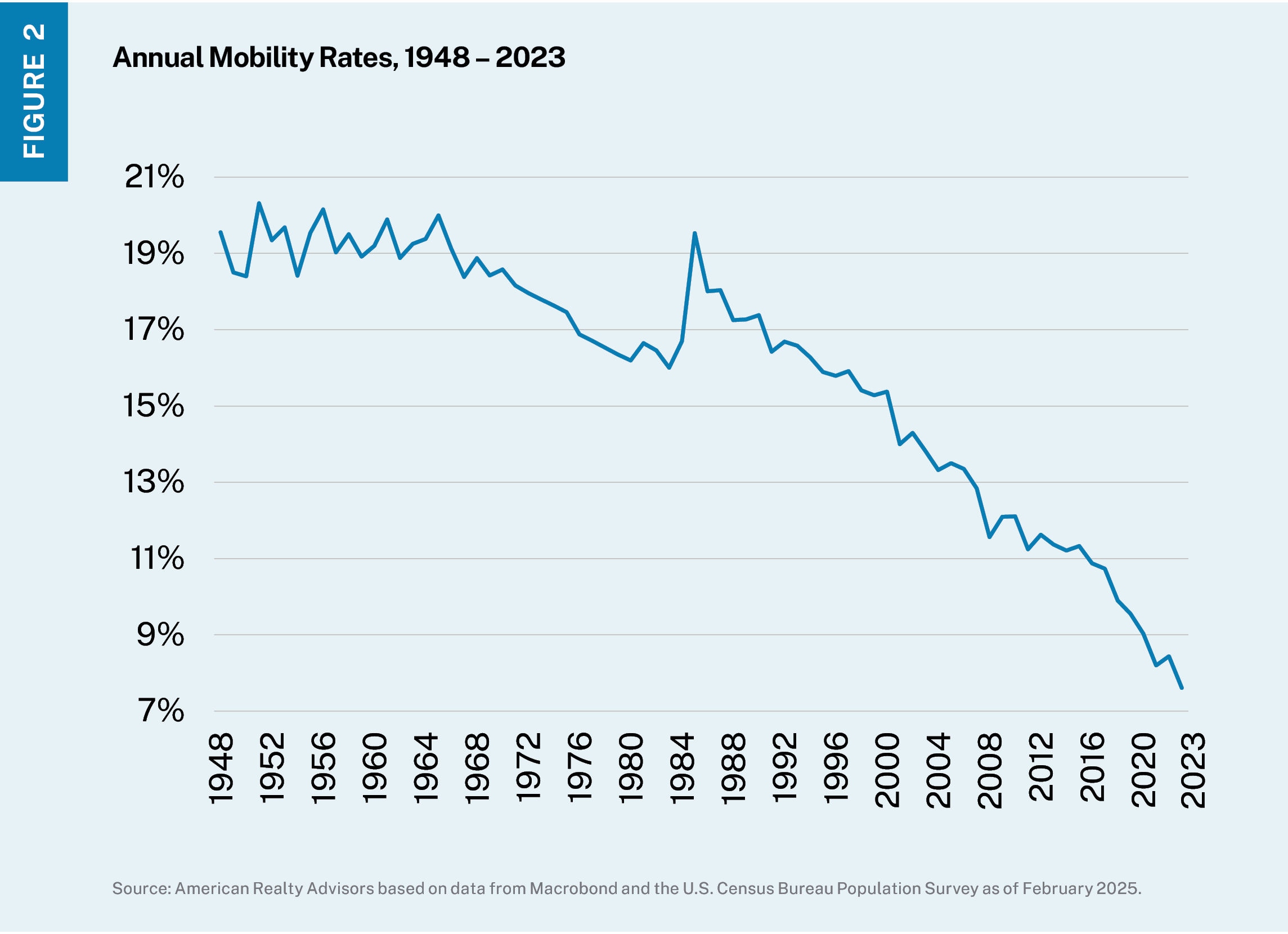

It is tempting to assume that if immigration slows, domestic migration will simply pick up the slack – that job growth will pull renters across state lines and keep demand humming. However, domestic mobility has been declining for decades (Figure 2). Fewer households are moving across state lines than in prior cycles, meaning the overall flow of movers is thinner. For multifamily owners, that means fewer renter households arriving from other states to backfill new deliveries.

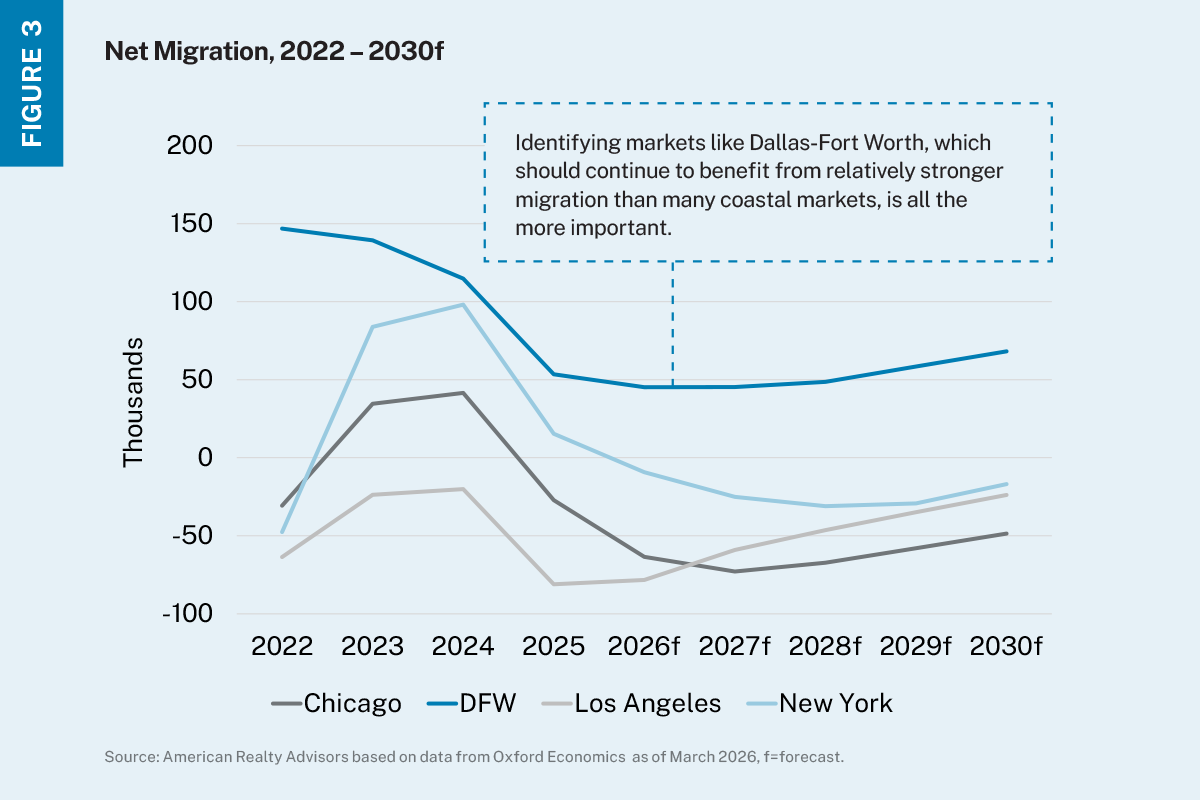

For instance, Florida and Texas, two of the biggest migration winners in recent years, are seeing inflows settle back from the unusually strong pace of the last cycle. That said, the core reasons people moved there – business-friendly environments, tax advantages, and lifestyle appeal – have not changed. These states are still likely to attract a meaningful share of domestic movers (see DFW example below). The difference is that the overall pool of movers is smaller, so the competition for each new resident is more intense.

For multifamily investors, this shift is not a signal of demand disappearing. Rather, it is a signal that broad demographic tailwinds can no longer do all the work. In the prior cycle, strong population growth made it easier for many markets to absorb new supply and support optimistic rent assumptions. Today, outcomes are likely to depend more on submarket selection, entry basis, pipeline awareness, and asset positioning. The opportunity set remains, but capturing it requires sharper underwriting and more localized conviction.

Lower overall population growth prospects are likely to be a nationwide factor in the cycle ahead, but not all markets will feel that pressure equally.

What makes Dallas-Fort Worth attractive: Dallas-Fort Worth continues to check many of the boxes that matter most for long-term apartment demand: jobs, affordability, migration appeal, and demographic depth. Its diversified economy helps support resilience, while no state income tax, warmer weather, and a relatively attainable cost of living keep the market attractive to younger households and employers alike.

Mid-Quarter Economic Pulse: Q1 2026